However, these figures are averages. There will be some winners and some losers with any sweeping change to the tax code. In particular, the limits placed on state and local tax deductions are leading even prominent Republican representatives to vote against the bill since theoretically reducing state and local deductions could hurt their constituency more than the other provisions help.

I’ve found the changes in the tax code to be difficult to explain in plain English. It might be helpful to walk through how the tax calculation is changing for specific taxpayers - and I’d like to start with me personally.

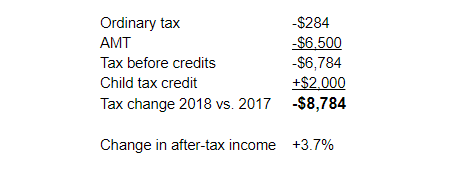

The deduction of state income tax is a particular concern for me in the State of New York, as I expect to pay more than $19,000 in state income tax in 2017, in addition to $14,000 of real estate taxes. In the old tax bill, I could deduct all $33,000 of payments against my federal income tax, reducing my taxable income dollar-for-dollar by that amount. In the new tax bill, only $10,000 of the $33,000 will be deductible. Adding all of this up, from 2017 to 2018 I expect to lose the following:

Those are big numbers! However, I’d benefit from other provisions of the bill. I receive a small but significant income stream from a rental property, and because my adjusted gross income is less than $315,000, I expect to receive the 20% pass-through tax deduction on this income. That will lower my taxable income by $4,200 relative to 2017.

Another huge factor: my wife and I welcomed our first child in February of 2017. Under the old tax system, I would not have received a child tax credit of $1,000 because our income is higher than the phase-out amount. However, the 2018 child tax credit has doubled to $2,000, and the income phase-out doesn’t begin until $400,000 of AGI. Credits count dollar-for-dollar against tax due, and as such this $2,000 credit is very valuable.

Yet the biggest single change to my personal situation is the change to how AMT (alternative minimum tax) is calculated. The AMT exemption figure has doubled, and isn’t phasing out until a married couple is earning $1,000,000 or more, helping to reduce the total amount of AMT paid overall. A greater change is that the factors that usually trigger AMT - state income tax deductions, real estate tax deductions, and personal exemptions - are either limited or repealed entirely. In 2017, I expect to pay around $6,500 of AMT, while in 2018 I expect to pay $0.

Putting it all together, here’s how I expect things to look like in 2018 compared to 2017:

There was a lot of concern from New York taxpayers about the loss of state & local deductions, but according to analysis based on my reading of the bill just about everyone will still see a tax decrease under the new bill. Here are a few additional examples, with and increasing level of complexity.

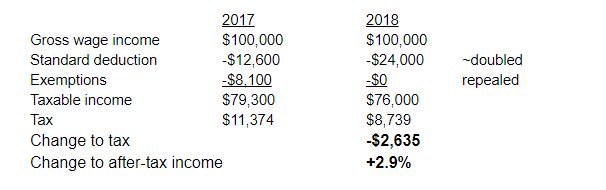

Let’s start with a married-filing-joint taxpayer - each person makes $50,000 of wage income - no kids - no property taxes or mortgage interest:

Here, increasing the standard deduction by almost 100% helps as such as compressing the 15% bracket to 12%.

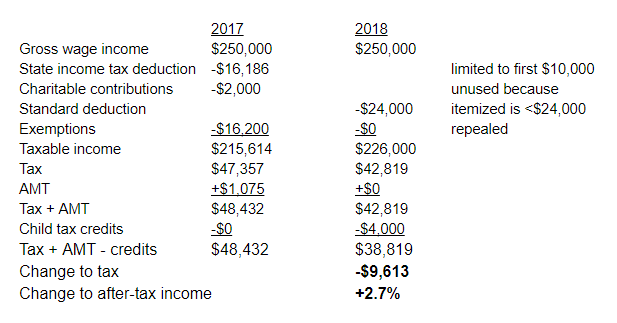

Let’s run the same analysis for a family of four (two kids age 10), with joint income of $250,000. Let’s assume that they live in New York, and also give $2,000 per year to charity.

A few things to note in this scenario. First, the charitable contributions help to reduce 2017 income tax (and AMT paid), but are not applicable in 2018 because the increase in standard deduction to $24,000 is higher than the sum of the taxpayer’s itemized deductions. The reduction in taxable income plus lower overall tax brackets (at the high end, 28% vs 24%) decrease taxes by about $5,600. AMT is triggered in 2017, adding $1,075 to their tax bill, but not in 2018. Additionally, this taxpayer with two kids under the age of 17, meaning they will receive enhanced child tax credits available for taxpayers who make up to $400,000 in 2018. Child tax credits in the prior system were phased out for taxpayers earning up to $110,000.

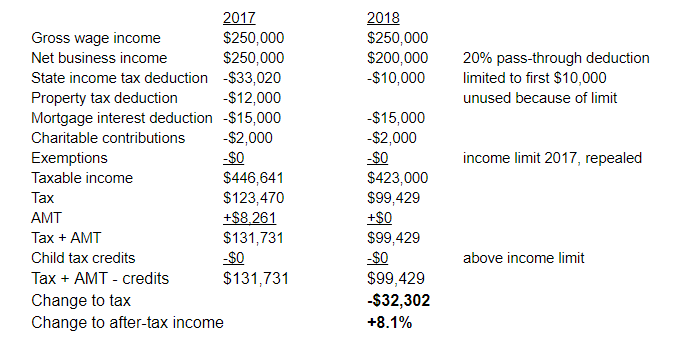

Lastly, let’s take a look at a taxpayer earning $500,000 per year - $250,000 comes from wage income as above, but then they receive an additional $250,000 in qualified business income eligible for the 20% pass-through deduction (likely rental real estate), two kids (age 10), and they own a house and pay $12,000 of property taxes + $15,000 of mortgage interest, with $2,000 of charitable contributions.

Here is where all of the goodies kick in: the taxpayer still itemizes, because state tax + real estate tax + mortgage interest + charitable contributions exceed $24,000, the taxpayer won’t trigger AMT, and even though their income is too high to receive the $4,000 of child tax credits, they will still see a $32,000 difference between their 2017 and 2018 tax bills.

Note that a large part of the savings above come from the complicated 20% pass-through deduction. If there was no pass-through deduction and the taxpayer earned $500,000 in wage income alone, the tax differential would be cut in half to $15,439, or +4.0%.

In conclusion, reading through the new tax bill and applying it to the scenarios above, I was hard pressed to find a way that the state and local tax limits would result in a tax increase from year-to-year. It is possible that a taxpayer who is currently itemizing deductions, who is not subject to AMT, and who is not receiving the additional child tax credits to see a tax increase, but it appears as though the majority of taxpayers that I work with will have some additional after-tax income to play with in the years ahead.

- Bill